Re-thinking pakistan’s rlng “crisis“ in the wake of war

Written in collaboration with Climate Action and Energy Access Institute (CAEA).

To understand the scale of the ongoing RLNG supply crisis in Pakistan in the wake of US- Israel aggression against Iran, we should resist being swept away by the theatre of disruption unfolding across the region. We need to take a step back and read the story in a more holistic manner - keeping context at the forefront.

What we need to remember, fundamentally, is this: RLNG - both as a commodity and as a fixture - was already a crisis for Pakistan long before the war.

There is, in fact, a good possibility that the force majeure declared by QatarEnergy could turn out to be a blessing in disguise for Pakistan, provided the policy response is deliberate, sequenced, and anchored in a new-age energy security paradigm.

Already, voices within the power sector and government forums are treating the QatarEnergy force majeure as a justification to accelerate Pakistan's reliance on alternative thermal options - including Gwadar Coal plant/imported coal and domestic Thar coal - at scale. (Dawn) (The News) This can be a costly and long-lasting mistake. The disruption did not create Pakistan's energy vulnerability; it exposed a system already burdened by overcommitted RLNG contracts (Business Recorder) (Energy Update), merit-order violations (Energy Update) (Express Tribune), and structurally declining gas demand. (The Nation) (CEDIGAZ) Our purpose here is to examine these pre-existing realities carefully and to press upon the government that the response to the presumed shortage must be driven by transparent evidentiary back-ups in a way that the country does not repeat the history again.

Overplaying its hand on Exploration & Production or constructing new coal fleets without accounting for changing and declining gas demand patterns and the availability of cheaper alternatives, risks once again locking the country into the practices of a bygone era. Our argument rests on the following three pillars.

The RLNG Experiment: Overbuilt, Overcommitted, and Overdue for Accountability

At the outset, we would like to remind readers that emergence of RLNG and its value chain was not purely an endogenous development. Major and well connected local energy conglomerates converged with the World Bank Group and its private Financing arm (IFC) to secure fundings and develop LNG import terminals. Terminals that sit on Pakistan's coast and, as we write, continue to collect around $ 15 Million per month in capacity payments even without RLNG although revisions are expected. The role of the MDBs in hurrying Pakistan into the fast tracked RLNG value chain must be seen for what it is. This largely irrational foundation must surface in analysis of the fact that RLNG power plants have: i. have never produced power at full capacity. ii. consistently drove merit order violations. iii. locked Pakistan into expensive power generation driving the electricity prices and iv. massive circular debt and gas losses keeping the country behind on the growth trajectory.

Furthermore, RLNG-based power plants have, for much of their operational life in Pakistan, been run in violation of the economic merit order, thereby driving up electricity tariffs. (Pakistan Electricity Review 2025).This is extensively documented in news reports and institutional publications, including repeated State of IndustryReports, which vividly capture NEPRA’s frustration with the compulsive operation of RLNG plants despite the availability of cheaper alternatives. The root cause has been long-term contracts with the plants and long term take or pay gas supply agreements with Gulf based QatarEnergy, a condition that has persisted in various forms and which we unpack further below. (Dawn).

““Another major contributor to the high cost of electricity generation is the operation of RLNG-based power plants having long-term supply contracts. These plants, due to the nature of their contracts, are required to operate in preference over other cheaper power plants. As a result, the system operator is required to compromise overall economic merit order operation of power generation plants most of the time.””

This pattern did not end in 2019. The same phenomenon reappeared in November 2025, when NEPRA Member (Development) Maqsood Anwar Khan again questioned CPPA-G on why RLNG-based plants rose from a reference share of 5.2% to an actual 21.59% of generation, while cheaper coal remained underutilized. The CPPA CEO’s response was structurally identical to explanations given in 2024: take‑or‑pay obligations, grid stabilisation needs, and proximity to load centres. The repetition indicates a systemic pattern, not a one‑off aberration. (Energy Update).

We recognise that system constraints have also contributed to forced dispatch — an issue articulated in detail in the State of Industry Report 2025 and the Pakistan Electricity Review 2025. However, our main point is that Pakistan may have sufficient alternatives including the domestic gas resources to meet much of the demand erstwhile met by RLNG in a more honourable and economically rational way - a proposition supported by both rising domestic reserve estimates per the HDIP Energy Yearbook 2024–25, the declining gas demand, and the documented suppression of local gas fields producing up to 400 MMCFD without holding anyone responsible to accommodate imported RLNG. But this also requires compliance with the merit order rules where possible, plus a transparent demarcation between system stability-based demands for RLNG power plants and contractual requirements-based forced dispatch - a distinction that ISMO's own revised Economic Merit Order implicitly surfaces. While this article cannot address that comprehensively, pushing the regulators and the Energy Division to provide a transparent assessment of how RLNG dispatch was being conducted. The AGP's Special Audit on the RLNG Supply Chain has already flagged lax demand forecasting before embarking upon the costly RLNG procurement.

Can local gas save the day?

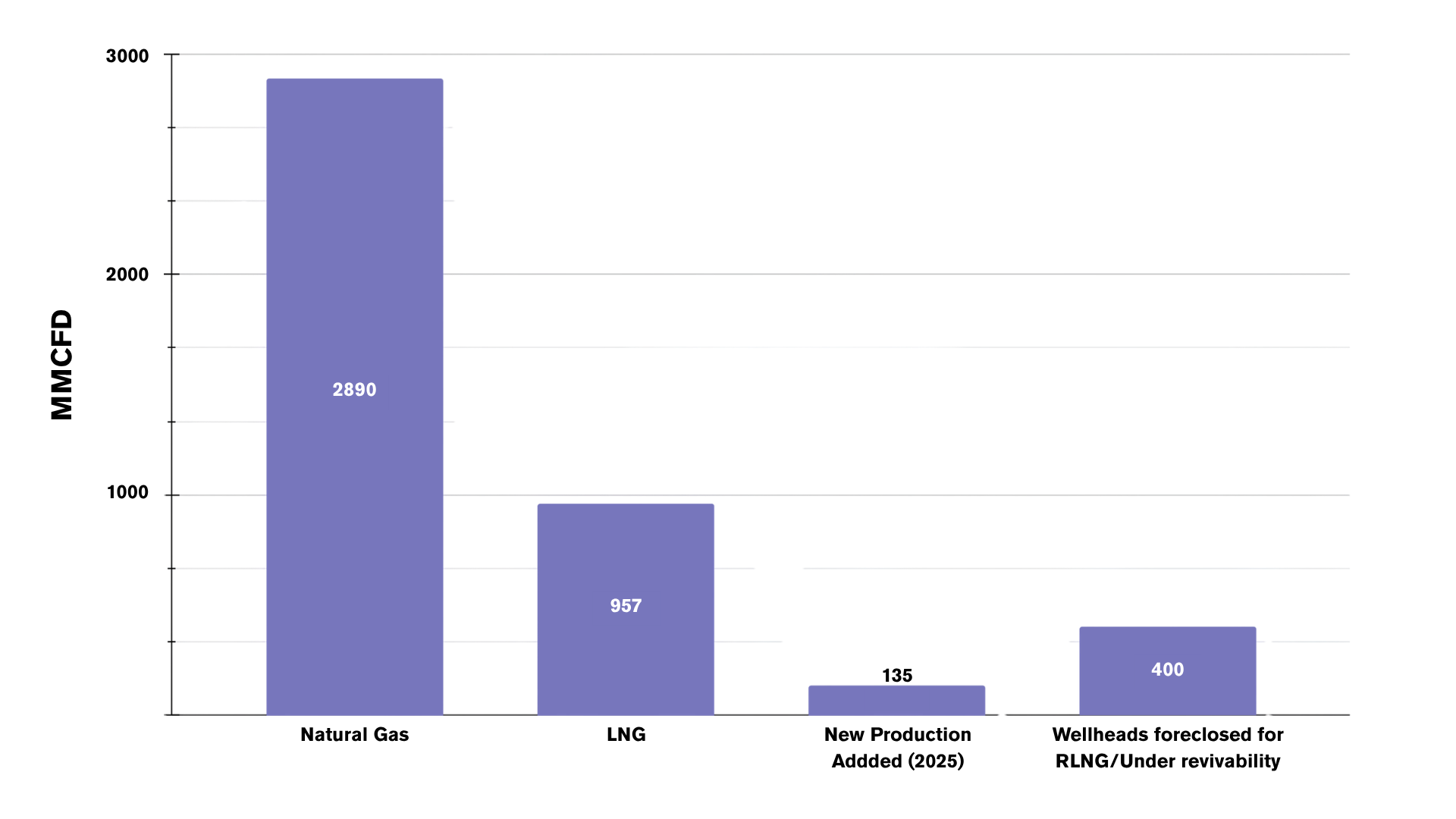

Available data confirms local gas curtailment due to forced diversion of around 58,177 BBTU in 2024-25 which increased further to 81,303 BBTU in 205-26 as quoted in SNGPL’s latest ERR to low paying domestic consumers led by skewed demand in the power and captive industrial sectors within the SNGPL system- a volume that constitutes half of the total power sector consumption of RLNG in 2024-25. When you read the graph below keep in mind how much of it was being diverted to low pressure networks and uses. During 2025, the diversion of RLNG to the domestic sector surged to 452 MMCFD over and above the power sector causing net revenue loss and spike in Circular debt (The News).

State of gas and RLNG Consumption (2024-25)

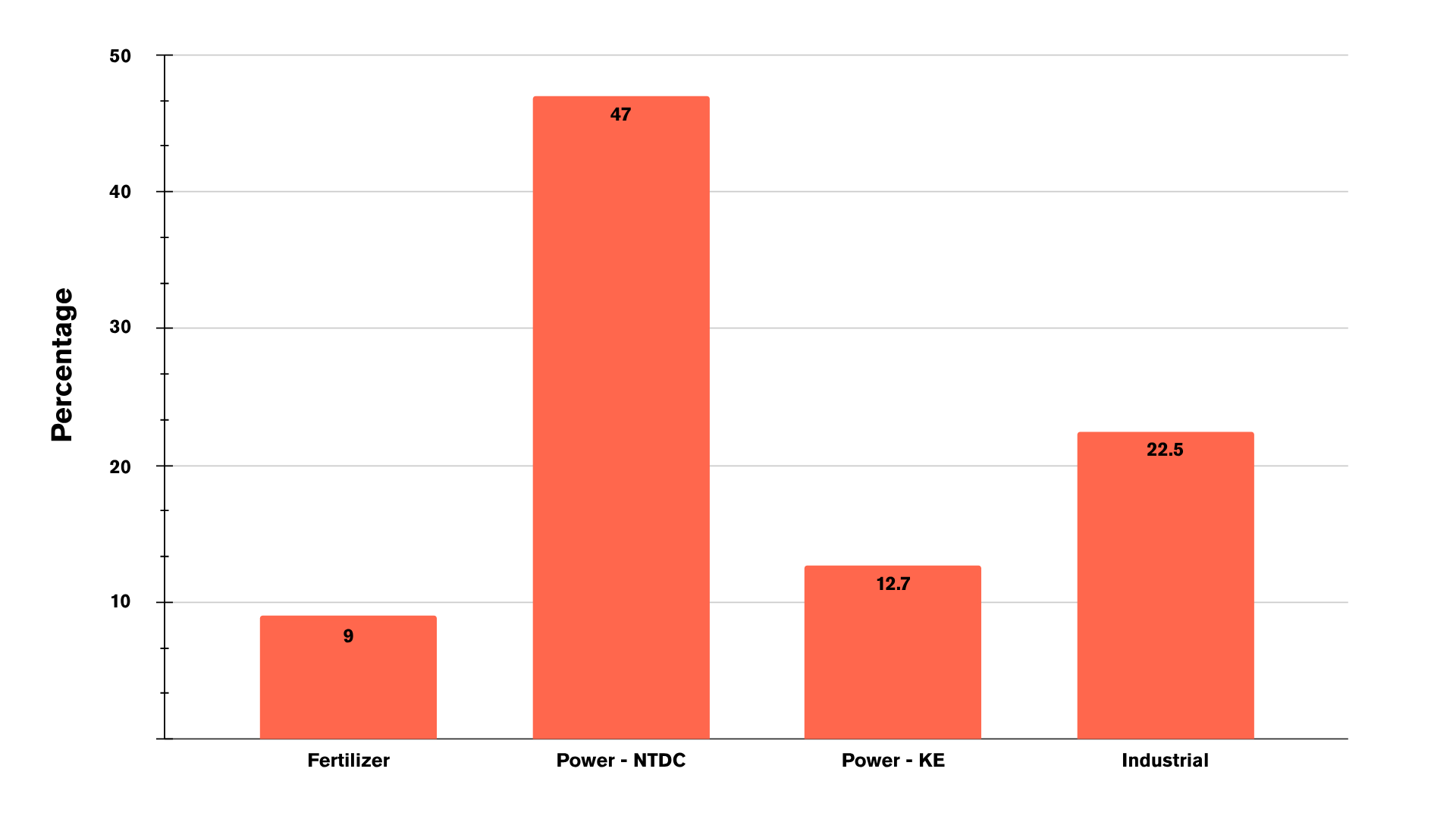

Sectoral Consumption of RLNG (2024-25)

From these graphs, we deduce that the quantum of RLNG used in the power sector along with the industrial sector approximately squares off with the total gas curtailed and added to the system.

The percentage shown in the graph above pertains to the 957 MMCFD that the system received in 2024-25.

When compared with the fact that many of the RLNG cargoes were renegotiated and diverted to the open market the total volume of RLNG in the system goes down dramatically. In short, both NGC and K-E consumed approximately 545 MMCFD in 24-25 an amount which equates with the volume curtailed at the domestic level.

We believe the total requirement will even come down further if we make a distinction between the quantum needed for the system stability vs the quantum combusted to meet the must-run obligations. It is the duty of the Regulator to make a clear demarcation to ensure the stability and legitimacy of the future planning process.

We can also state with confidence that the de facto “must‑run” status of RLNG-based power plants has been significantly diluted or removed. (GetTransport blog) (Geo News). There is a larger story here about how this configuration distorts the distribution of costs and liabilities, and how NEPRA’s frustration is rendered toothless when those who contract RLNG volumes and those who dispatch them operate in institutional silos. That story, however, must be left for another day.

For now all we want to say is that the diversion ofRLNG to the domestic sector was caused by the failure of the power plants to absorb the volume they had committed. Therefore, the responsibility of bearing that burden must have been on the soldiers of the power sector and not the petroleum division. For reference, read the delta between how much RLNG costed vs how much the domestic sector pay for it:

“The current domestic gas tariff averages Rs1,250 per MMBTU, while the RLNG tariff is Rs3,600 per MMBTU, creating a loss delta of Rs2,350 per MMBTU. A senior Petroleum Division official estimates the diversion loss from November 2024 to March 2025 at over Rs200 billion, further adding to the gas circular debt. In the last two years, the circular debt for the gas sector increased from 2000 Billion rupees to 3,200 Billion rupees in just two to three years. Addressing this through revenue requirements could lead to sharp increases in gas tariffs.” (Energy Update)

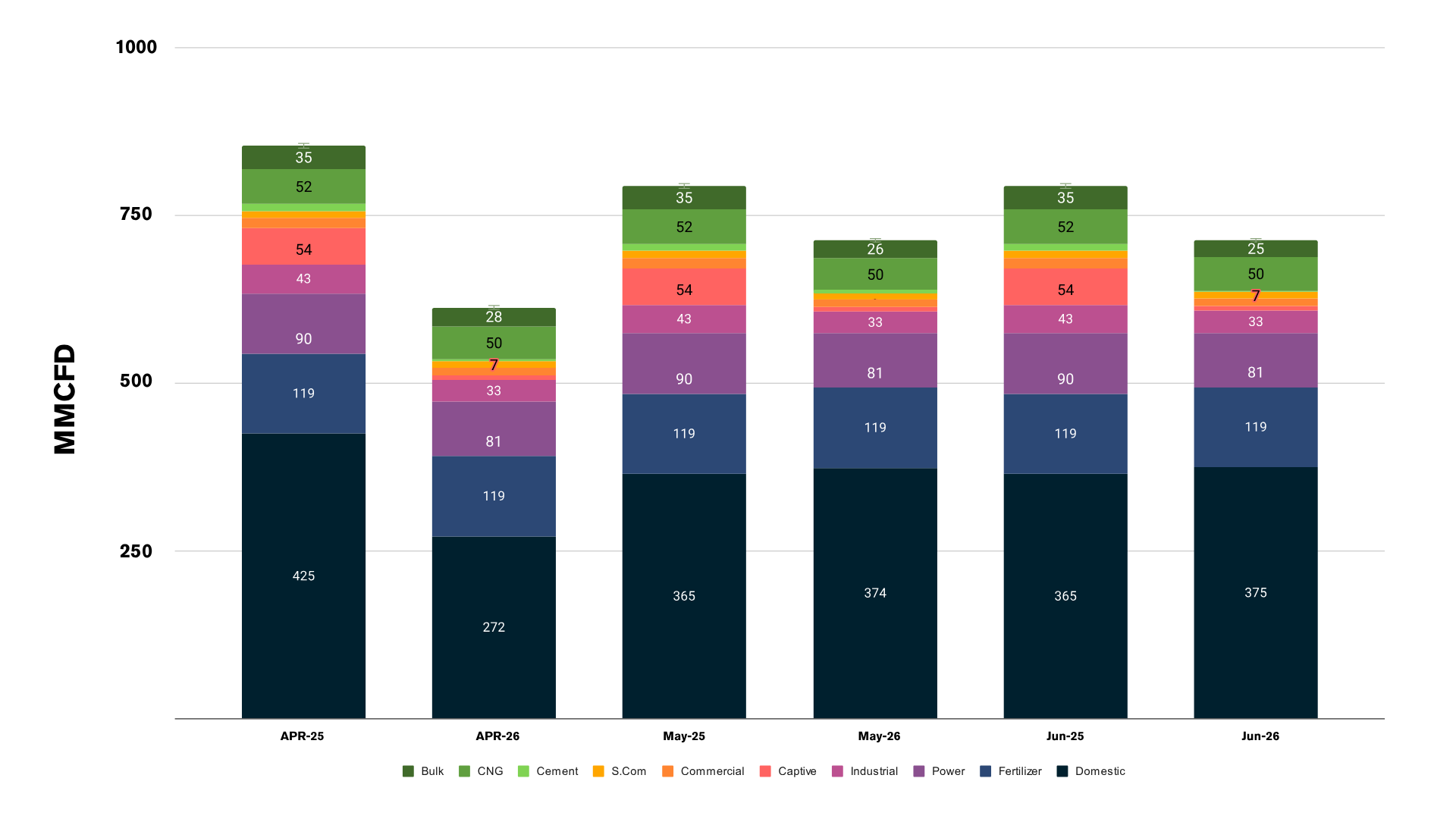

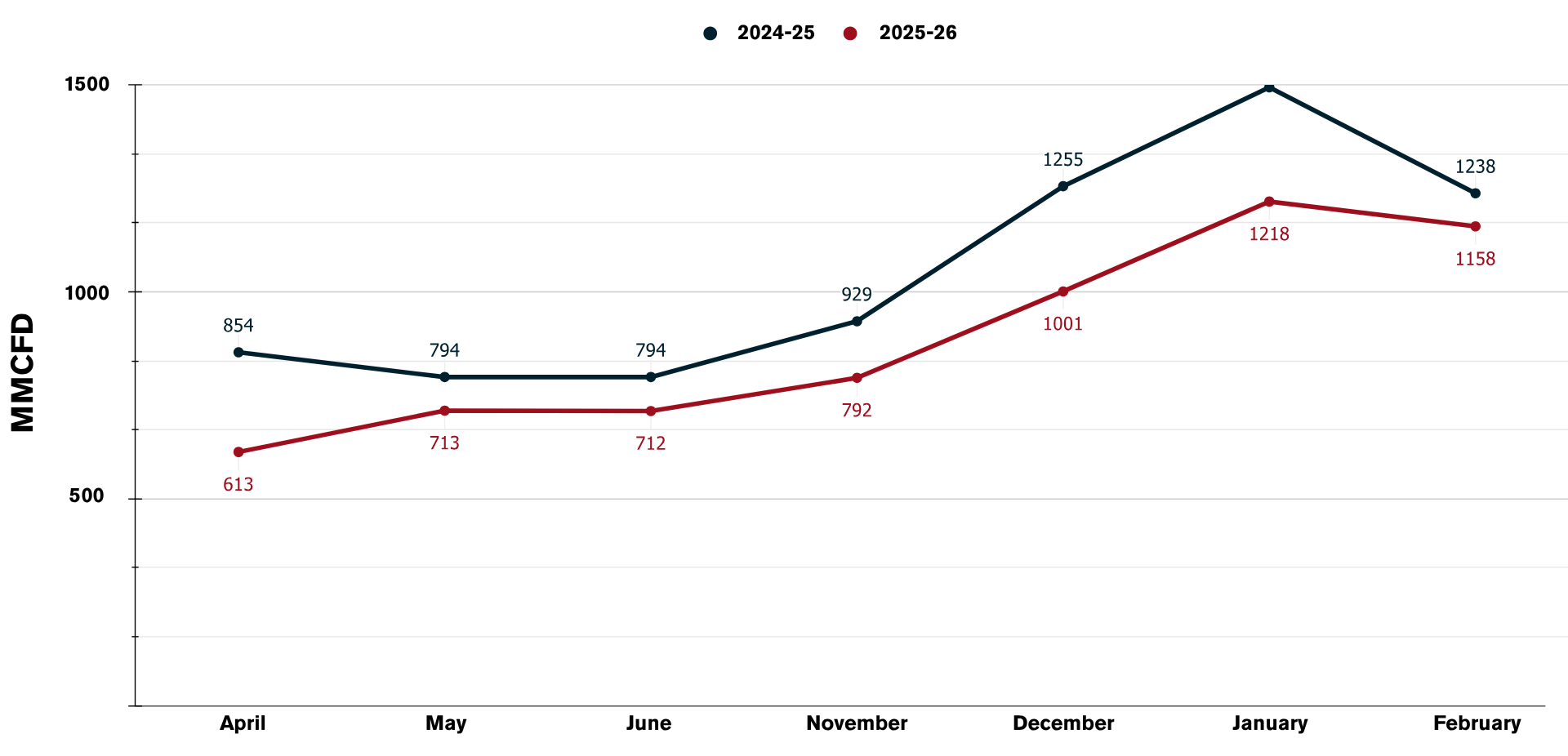

Mid-summer sectoral gas allocations in sngpl april-may-june (2024-25 and 2025-26)

These pre-war projections reflect the organic decline in many of the erstwhile uses.

The last section of this report explains the reasons for the structural decline. For the domestic sector, the decline is also reflective of change related to reduction in demand for gas during the summar.

The graphs also show how summer allocations create significant space for rationing gas allocations away from the domestic sector and prioritize strategic and central power sectors for gas supplies.

The graph shows almost 130 MMCFD decline in the overall demand for gas in the summer, marking a significant decrease in the pre-war period.

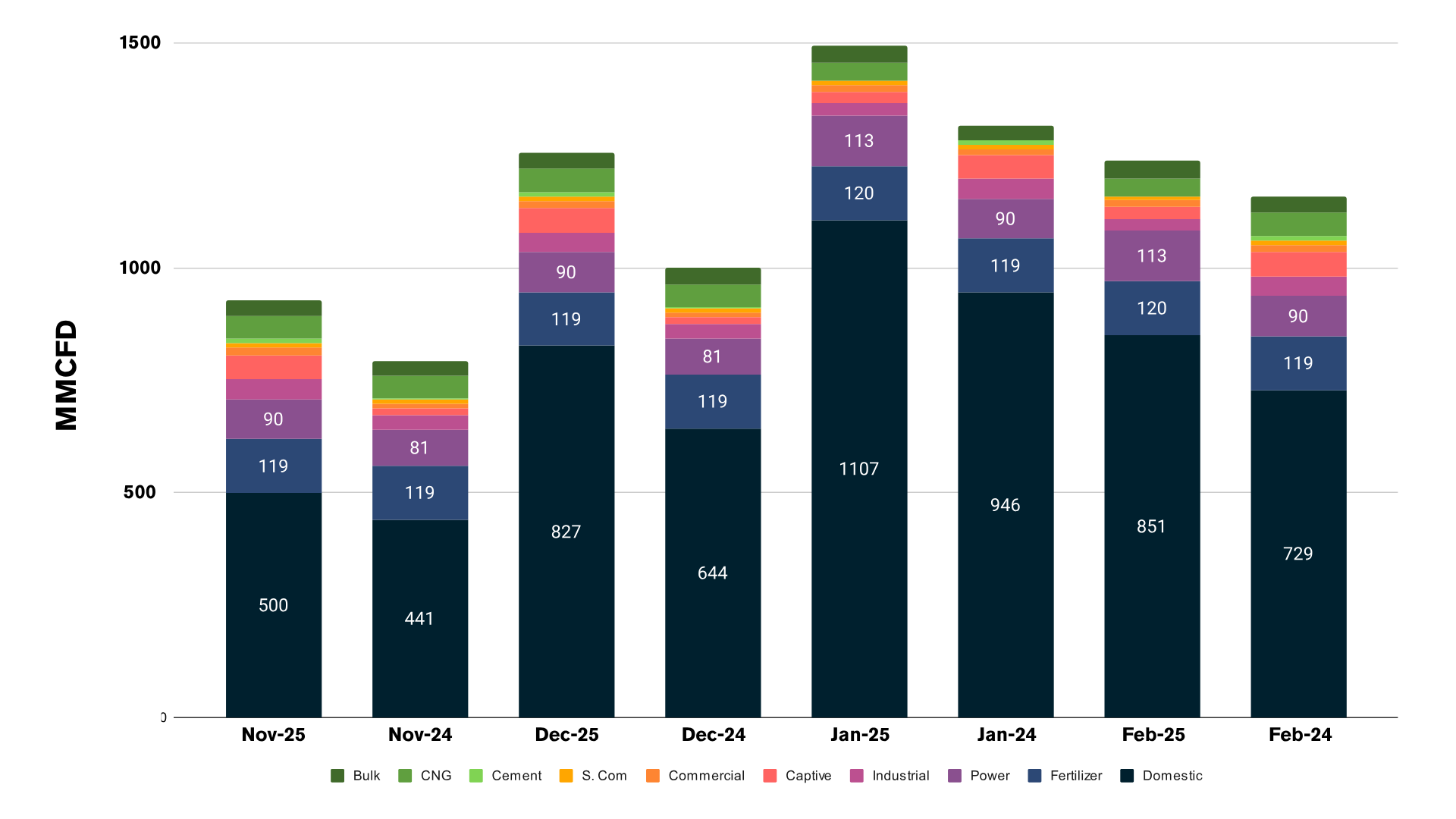

Winter Sectoral gas allocations in SNgpl nov-dec-jan-feb (2023-24 and 2024-25)

As stated above, the sectoral demand destruction of gas on account of higher tariffs, solar rush and IMF conditionalities bears out in the winter allocations of 2024-2025, showing declining allocations between 100 to 200 MMCFD across peak winter consumption months. The difference in demand quantum during summer and winter is important to bear in mind.

Year-on-year change in sngpl gas demand

The change is not miniscule. Again this reduction was projected during the pre-war period and not influenced by the current ‘disruption’ narrative we see pedalled today. Ultimately, it points to the need for careful calculations around demand forecasting.

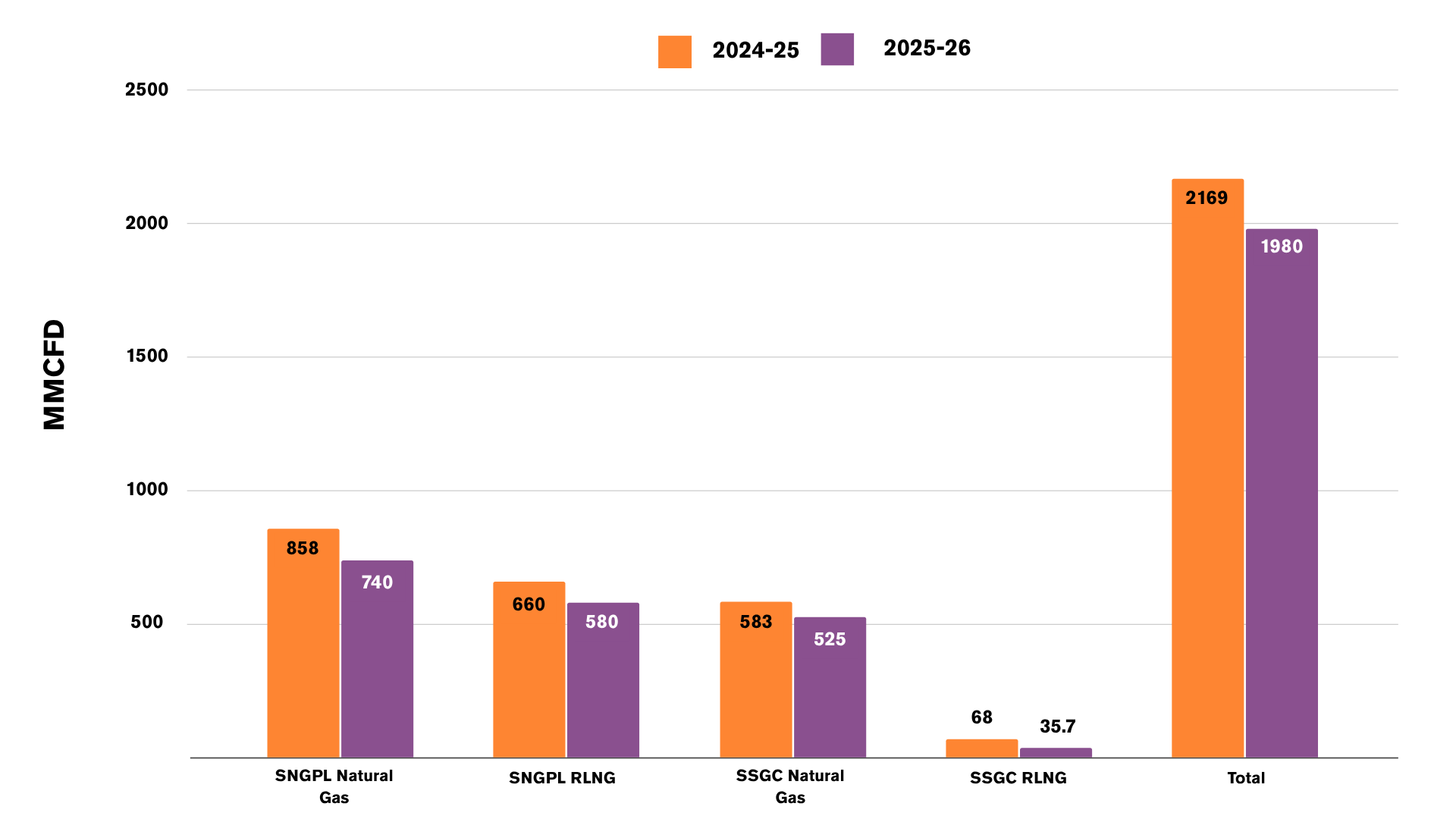

Total natural gas and rlng sales

Note: While the graph is self-explanatory. We add some further layers and actions to this. The major consumer of RLNG was SNPLG which necessitates that the consumers in the North, particularly those in Punjab, expedite their transition to cleaner sources. The Punjab Climate Policy is particularly relevant to revisit. The 2035 target (500 industrial units shifted to cleaner sources) is revised to earlier targets. Secondly, SNGPL and SSGC are deeply connected and have been using the same system for the delivery of gas and RLNG without any distinction.

Therefore, the replacement of RLNG with gas does not constitute any logistical problems for Pakistan in terms of supply reserves.

Renegotiating RLNG - an incomplete project saved by total disruption

We now explain the scale of the pre-war RLNG glut and its impacts particularly the government’s (particularly the Petroleum Division’s) efforts to renegotiate overcommitted RLNG capacity, the volumes actually utilized by the power sector, and the interactive impact on domestic gas resources and their ability to meet demand.

First, the federal cabinet approved the diversion of 24–29 surplus Qatari cargoes in 2026 under the Net Proceeds Differential (NPD) arrangement. This represents roughly 22.2% to 26.9% of the annual volume contracted with Qatar under long-term RLNG agreements. (Business Recorder). The government claims savings of Rs 1 trillion translating into 3,586,230,000 USD from this negotiation alone. What is particularly telling is that even after the Annual Delivery Plan had been finalised, the Power Division once again conveyed to the Petroleum Division that the power sector would not consume nine more LNG cargoes - worth approximately $270 million. (The News). According to Sui Northern Gas Pipelines Limited (SNGPL) and Pakistan State Oil (PSO), the total number of surplus cargoes projected between July 2025 and December 2031 stands at approximately 177, equivalent to around 24 cargoes per year on average. (The Express Tribune). Earlier, in 2024, the government had already secured a concession from Qatar to defer five cargoes from 2025 to 2026. (Reuters). These realities need to be properly assessed to determine the true demand for RLNG within the system. Can it be as low as the 5% reference value indicated in the State of Industry Report, or is the actual structural demand meaningfully higher?

The scale of overcommitment becomes clearer when we look at how much RLNG the power sector actually used during peak periods. Out of the total volume committed on SNGPL’s system, the power sector could consume only about 600 MMCFD, falling short of the contracted 800 MMCFD. At the same time, the export sector’s RLNG consumption plunged from 350 MMCFD to just 100 MMCFD due to rising costs and IMF based conditionalities. ISMO’s dashboard on RLNG for 2025 suggests that the total volume of electricity produced on RLNG from May to September was about 16000 GWh- A volume that could be met if 400 MMCFD of the domestic gas could be diverted to that excluding the losses and other system constraints. (ISMO). But we would again emphasise on the demarcation between system constraints based generation vs. contractual requirements based generation.

Furthermore, when we connect this under‑utilisation to the impact on domestic gas fields, the picture becomes stark: the RLNG glut effectively forced the shutdown of local fields producing around 400 MMCFD. As one report notes:

“A significant reduction in the use of imported Regasified Liquefied Natural Gas (RLNG) by Pakistan’s power sector has led to the shutdown of local gas fields producing up to 400 million cubic feet per day (MMCFD), sparking concerns over long-term damage to the country’s energy infrastructure.”

The government applied the same logic with ENI; that episode follows the same pattern and need not be detailed here. What matters is that, even after these negotiations, RLNG remained in substantial surplus. This is most clearly evidenced by a highly controversial step: lifting the moratorium on new domestic gas connections specifically to absorb RLNG.

To manage the glut, the government adopted several desperate schemes. Most notably, OGRA approved Rs 6.1 billion for SNGPL and SSGC for new RLNG-based domestic gas connections, under their Estimated Revenue Requirement petitions for FY 2025–26. Under this approval, SNGPL was to offer 300,000 domestic RLNG connections, and SSGC 50,000. This measure alone illustrates the extent of the problem: even after diverting roughly 22% of committed volumes under the NPD arrangement, the government still did not know what to do with the remaining RLNG. The economic folly and future stranding risks associated with this step could fill an entire separate analysis. It will be instructive to see whether, and how transparently, the government rolls back these measures in the wake of LNG supply closures.

Since a significant portion of RLNG was in process of being diverted to our domestic sector, the disruption might expose the folly of such a measure. Instead of pushing domestic systems to the alternatives and subsidising the transition, they were locked into an energy pathway premised on RLNG flow in their systems indefinitely.

It is important to note that we are not referring here to schemes within 5 km of gas fields, for which the ECC recently approved technical supplementary grants (TSG) of Rs 3 billion to be implemented by SSGC and SNGPL. Those targeted schemes are more consistent with CSR policy and equity principles.

In parallel, the Energy Yearbook 2024–25 by the Hydrocarbon Development Institute of Pakistan reports that Pakistan’s recoverable natural gas reserves have increased significantly, from 18.5 TCF to 23.3 TCF, owing to new discoveries and reserve re‑evaluations. These figures suggest that the country may no longer need RLNG volumes on the scale previously contracted, at least in the long term. When combined with structurally declining demand (discussed below), increased domestic gas availability, and ongoing solarisation, this trend offers a substantial cushion against RLNG disruption and creates an opportunity to save billions in foreign exchange - resources that could be reallocated to build resilience and genuine energy security.

If Pakistan were to move away from RLNG and towards domestic natural gas for power generation, the savings would be massive. Based on the State of Industry Report 2025, the total generation via RLNG in the FY 2024-25 was 27.97 TWh. Assuming fuel cost prices of 20.55 Rs/KWh for RLNG and Rs 13.80 /KWh for domestic gas, as given in NEPRA’s Fuel Charges Adjustment for December 2025, there is a potential for Rs 188.7 billion in energy price savings if a 100% of the RLNG load is shifted to domestic gas. The following table models how much savings would be accrued if a certain percentage of the expensive RLNG production were shifted towards cheaper domestic gas.

Structural Demand Decline and the Shift Away from Gas

Without delving into the full implications of Thar coal, nuclear expansion, and the large-scale solar build‑out - which have been discussed elsewhere - we want to underline how tariff rationalisation and structural changes in electricity consumption have reduced Pakistan’s demand for gas.

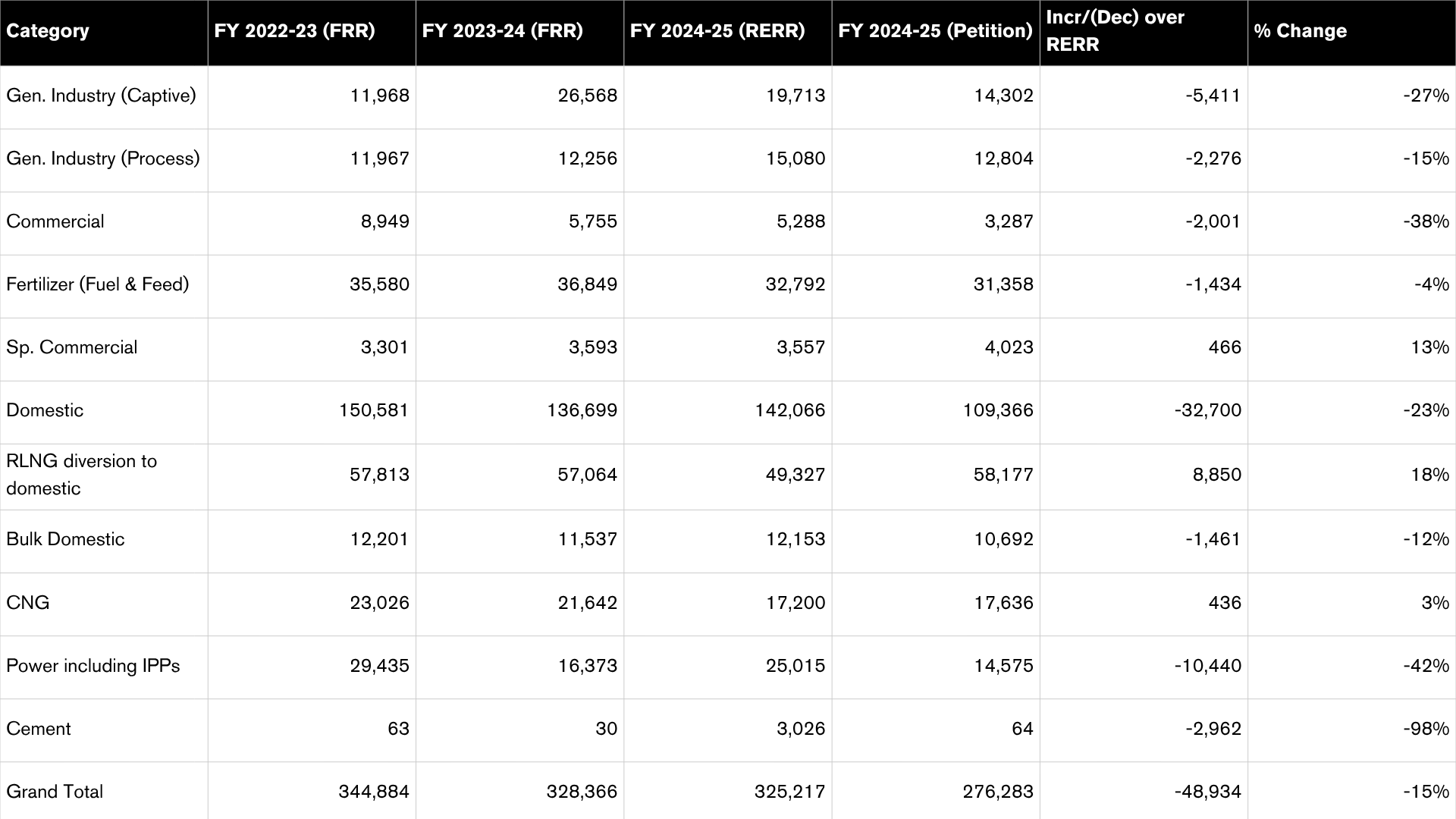

Under the IMF programme, tariff rationalisation measures and the forced migration of captive power (including fertiliser) onto the grid through hefty tariff add‑ons have significantly reduced gas demand. OGRA’s final determination for FY 2024–25 shows a 15% decline in SNGPL’s sales volumes. SNGPL’s own data for the domestic sector confirms a broad-based fall in gas consumption. While the graphs above explain the structural decline, we reproduce a screenshot from one of the OGRA’s decisions as well reasserting the same proposition- that demand reduction has kicked in.

In parallel, the expansion of solar capacity has enabled a shift away from gas at a scale for industries that cannot be understated. A Bloomberg article published on 23 March 2026 provides a telling example from Pakistan:

““The Chief Financial Officer of Pakistan’s Fauji Cement Co. installed its first solar array in 2019 at Jhang Bhatar, about 50 kilometers (31 miles) west of the capital Islamabad. There are now 69 megawatts of panels across the company’s five main sites, at least twice what Tesla Inc. appears to have on the rooftops of its gigafactories in Nevada and Texas. They contribute about 23% of the company’s electricity, with a further 35% coming from recovering waste heat from its coal-fired clinker kilns.””

The same trend of decreasing demand was notified by OGRA in its latest SSGC determination. In our estimation, removing the 523 BBTU of the CNG stations approved by OGRA for SSGC and rationing almost equal amount of indigenous gas from the 26000 BBTU allocated to captive power, the SSGC can be deemed to easily make up for the absent 13000 MMBTu of RLNG as per the SSGC Review of Estimated Revenue Requirement (RERR) for 2025-26.

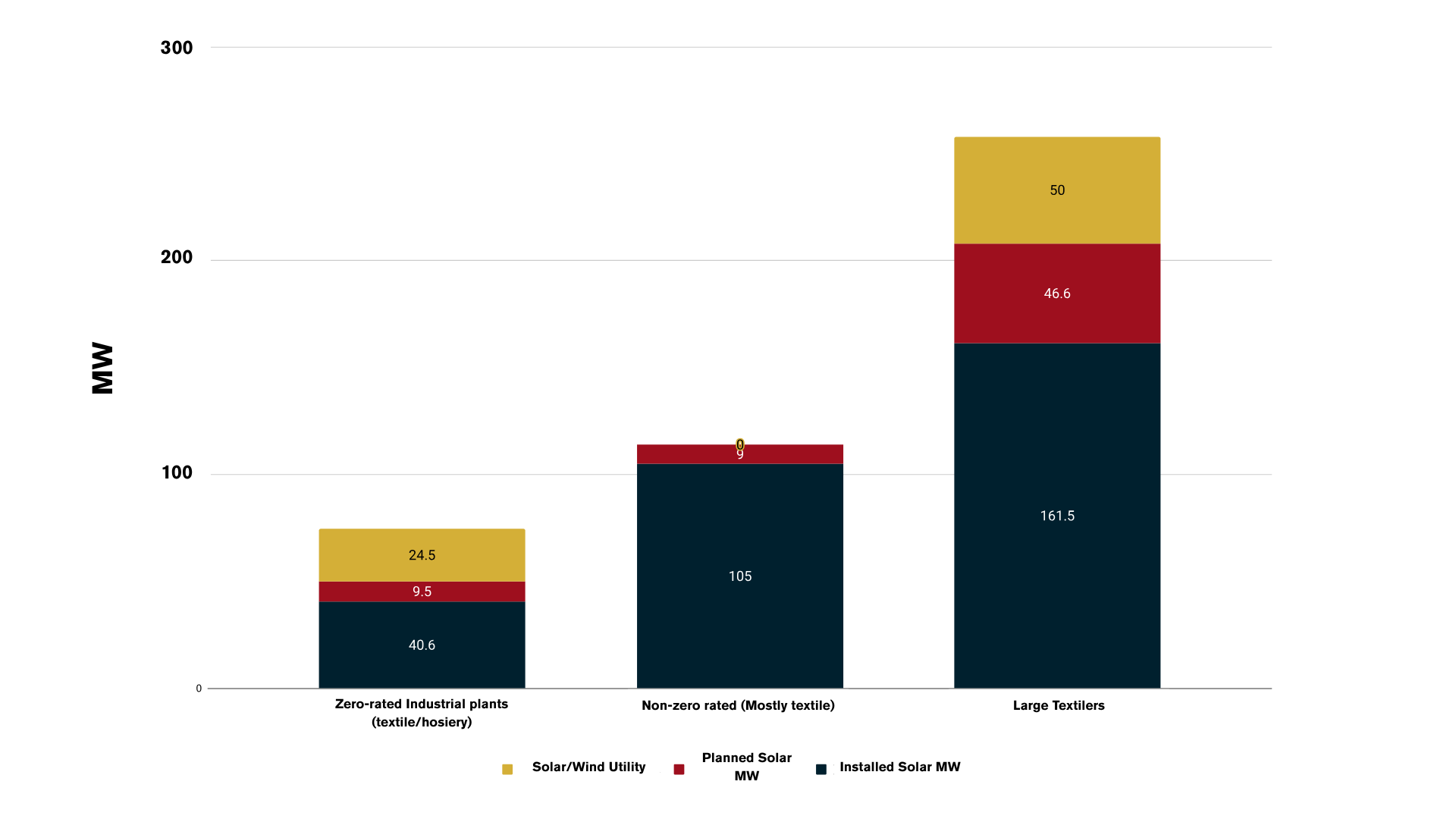

Industrial consumers like these as well as the large textile owners in SNGPL areas mainly consumed RLNG imported from the Persian gulf. Our calculations suggest that Pakistan's major 35 textilers had installed around 400 MWs of Solar and wind capacity by early 2025, not to mention the many other big and small units emulating the same at varying pace. Their transition to solar and waste‑heat recovery thus has a direct corollary: more gas becomes available for the power sector, easing the pressure on Pakistan’s external account.

Installed and planned Renewable energy in captives

Taken together, the reduction in gas demand, the prospects of increase in domestic gas, and the already-documented surplus of contracted RLNG suggest that the current force majeure is not simply a supply shock. It may, if handled with clarity and intent, become the trigger for a long‑overdue rebalancing of Pakistan’s gas and power system.

We end this article with the following note:

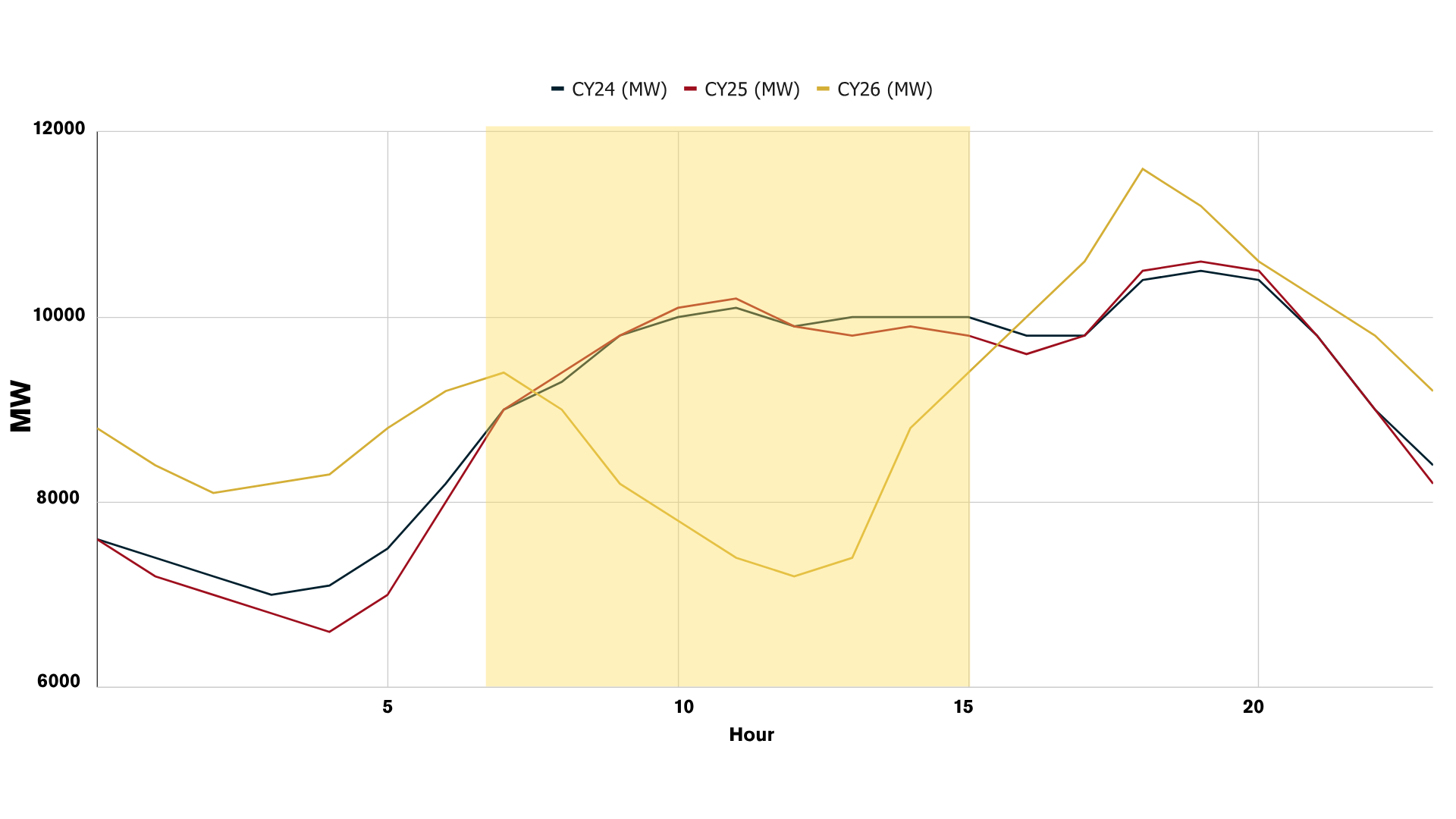

Demand for gas fluctuates a lot during summer and winter. It goes up in winter by several notches but goes down in summer particularly for the domestic sector. This fluctuation is helpful as the demand for gas load for the power plants is more in summer. Secondly, we are not claiming that the complete disruption in the supply of RLNG will cause no trouble whatsoever whether it be winter or summer- not at all. Our main purpose was to show how an in-depth accounting of pre-war scramble to get rid of RLNG cargoes in conjunction with the look at the availability of gas in the system, the possibilities of revivability of the wellheads foreclosed to make room for the costly RLNG and the structural decline in demand along with the possibility of other factors like solar rush etc might blunt the open calls for either the imported coal lock-ins or massive investments in local coal. A final caveat against the imported coal argument is that a significant surge in power demand on the Pakistani grid happens between very fast intervals, on hourly basis and emerges suddenly in the evening. A structural problem might be the impossibility of ramping up coal-based power plants on a daily basis to meet the massive demand surges.

An integrated assessment will allow us to think more about the new age energy security and resilience paradigm which is more supple, flexible, cleaner and equitable.

Hourly Electricity Demand Profile (MW) for february

Authors

Muhammad Abdurrafe from Alternative Law Collective

Email: mabdulrafe@gmail.com

Kamran Khosa from Climate Action and Energy Access.

Email: kamrankhosa@gmail.com